Macro back in the driver’s seat

ANTHONY SAGLIMBENE – CHIEF MARKET STRATEGIST, AMERIPRISE FINANCIAL

WEEKLY MARKET PERSPECTIVES — September 8, 2025

The S&P 500 Index posted its fourth weekly gain in the last five, while the NASDAQ Composite finished higher last week for the first time in three weeks. Throughout the week, investors looked through softening labor data, including a weaker-than-expected August nonfarm payrolls report on Friday, largely because prospects for additional Federal Reserve rate cuts by the end of the year have increased.

Fresh updates on inflation this week could help inform rate cut expectations and whether investors' assumptions on an increasingly dovish Fed are the right call.

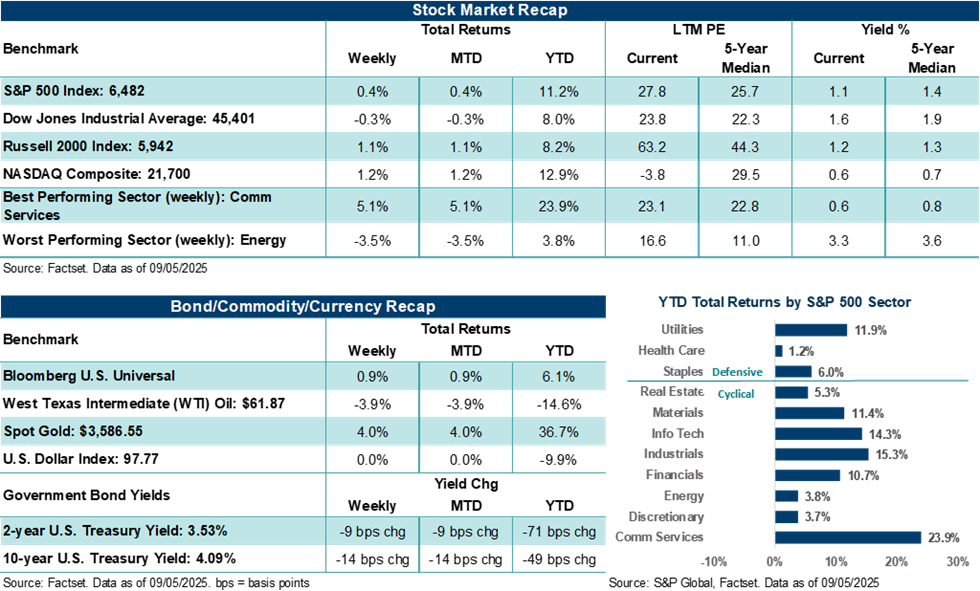

Last week in review:

-

The S&P 500 Index rose +0.4%, hitting a fresh new high on Thursday.

-

The NASDAQ Composite gained +1.2%, fueled by a +10.4% gain in Alphabet on a better-than-feared antitrust ruling.

- The Russell 2000 Index (+1.1%) and Dow Jones Industrials Average (-0.3%) posted mixed performance on the week. Strong gains in the Russell over recent weeks, on prospects of lower interest rates, have helped the small-cap barometer catch up to the Dow on a year-to-date performance basis.

- The 2-year U.S. Treasury yield hit its lowest level since April and one of its lowest points in the past three years.

- Gold finished at record levels, the U.S. Dollar Index was flat, and West Texas Intermediate (WTI) crude moved down on OPEC+ headlines pointing to further output increases.

- Employment data throughout last week pointed to a softer labor backdrop, and one where the Federal Reserve may have more room to cut rates than many investors assumed. The July Job Openings and Labor Turnover Survey showed job openings contracting more than expected. In addition, August ADP private payrolls (+54,000) missed estimates as well, with job gains deteriorating meaningfully from the +106,000 level in July.

- Fresh August looks at manufacturing and services activity showed the usual story of manufacturing trends stuck in contraction, while services activity continues to trace expansionary levels and drive economic growth.

“Investors are navigating an evolving macroeconomic landscape, balancing solid earnings growth and AI tailwinds against weaker employment trends, still elevated inflation, trade uncertainties, and the potential for disappointment if the Fed's data-dependent approach tempers the pace of rate cuts now baked into current expectations. And if growth and employment fade more than expected, or inflation turns north again, we would expect to see greater equity volatility across the market if stagflation anxiety rises.”

Anthony Saglimbene - Chief Market Strategist, Ameriprise Financial

Jobs, inflation, and the Fed are back in the driver's seat as investors look to navigate a complex environment.

Last week's market developments continue to paint a nuanced picture for investors, with last Friday's August nonfarm payrolls report sitting at the center of attention ahead of this week's inflation updates. The U.S. economy added just +22,000 jobs last month, well below expectations, marking a continued slowdown in labor market momentum. The unemployment rate ticked higher to 4.3% from 4.2% in July. Job revisions to prior months' data revealed a net reduction in job growth, reinforcing the narrative of a labor market that is beginning to stall. Private sector hiring remained narrow and concentrated in healthcare and social assistance. Government, manufacturing, and construction all shed jobs in August, and the average workweek edged lower. Bottom line: The overall pace of hiring in the U.S. is now running at less than half the level needed to absorb new labor force entrants, even accounting for lower net immigration, which is a worrisome development should labor trends remain soft or weaken further. In our view, employers in aggregate likely view current labor dynamics as a "no-hire/no-fire" environment and one where trade, immigration, and AI integration are clouding employment decisions at the moment.

Notably, the softness in employment is occurring alongside resilient services sector activity, as the August ISM Services Index surprised to the upside and reached its highest level since February. New orders rebounded sharply, inventories rose modestly, and prices paid eased slightly but remained elevated. However, employment within services contracted for the third consecutive month (an additional sign of labor stress), and company commentary continues to highlight tariff-related cost pressures and pre-holiday inventory builds. On the manufacturing side, the August ISM Manufacturing Index remained in contraction for the sixth straight month, missing estimates, but improved slightly over July levels.

Against a backdrop of mixed economic data last week, the market now expects a more dovish Federal Reserve heading into year-end. Fed officials, including Governor Waller, reiterated last week before the nonfarm payrolls report on Friday that rate cuts are likely in the coming months as labor risks increase. The combination of softening labor trends and persistent inflation (still well above the Fed's 2% target and likely to be pressured higher by tariff pass-through effects over time) has raised the specter of stagflation, though not in the severe form seen in the 1970s. The upcoming CPI and PPI reports this week will be critical in shaping the Fed's next steps, as policymakers weigh the risks of easing too quickly against the need to support a labor market that is losing steam. Bottom line: Market odds currently see a 100% chance of a Fed rate cut this month, with a small constituent seeing an outsized 50-basis-point cut on September 17 within the realm of possibility. From there, the market is pricing in additional rate cuts at the October and December meetings, which, in total, from now until year-end, could see as much as 75 to 100 basis points pulled out of the fed funds rate.

That said, equity markets have remained incredibly resilient given the unknowns, with the S&P 500 Index hitting a new all-time high last week and risk appetite now supported by expectations for easier monetary policy. Importantly, Big Tech continues to hold its ground, despite some recent bumps, particularly in Communication Services, as favorable legal outcomes for Alphabet and ongoing AI infrastructure spending by hyperscalers underpin sentiment. However, market concentration and elevated valuations leave stocks sensitive to shifts in sentiment, especially as the next wave of corporate earnings won't begin until mid-October. Bottom line: Investors are navigating an evolving macroeconomic landscape, balancing solid earnings growth and AI tailwinds against weaker employment trends, still elevated inflation, trade uncertainties, and the potential for disappointment if the Fed's data-dependent approach tempers the pace of rate cuts now baked into current expectations. And if growth and employment fade more than expected, or inflation turns north again, we would expect to see greater equity volatility across the market if stagflation anxiety rises.

Yet, we believe last week's data also helps support a guarded but still positive investment outlook with softening labor conditions and resilient services activity likely giving the Fed flexibility to adjust policy rates lower to support growth. Of course, by how much and how fast remains open for debate. Thus, market direction over the near term is likely to be influenced by incoming inflation data this week and the Fed's ultimate response to a complex mix of slowing job growth, persistent price pressures and ongoing trade uncertainty.

The week ahead:

-

August looks at NFIB Small Business (Tuesday), the Producer Price Index (Wednesday), Consumer Price Index (Thursday) and a preliminary September read on University of Michigan consumer sentiment line the economic calendar.

-

Notably, August consumer inflation is expected to tick higher to +2.9% year-over-year from +2.7% in July, while core CPI is expected to have held steady last month at +3.1% on an annualized basis. Inflation updates that come in largely as expected this week could keep small odds for a 50-basis point rate cut at next week's Fed meeting on life support. However, hotter-than-expected inflation across consumer and/or producer measures this week would likely throw cold water on the idea that the Fed is considering an outsized September rate cut.

- On the Washington front, headlines could continue to center on trade, after the Trump administration last week asked the Supreme Court to overturn an appeals court decision that found most of President Trump's tariffs on imports from other countries are illegal. According to the Tax Foundation, if the Trump administration tariffs are struck down by the Supreme Court, 70% of U.S. goods imported into the U.S. that are currently impacted by the duties would fall to roughly 16%. That said, over the weekend, White House officials expressed confidence the Supreme Court would ultimately rule in the President's favor, saying it has other legal authorities it can pull to apply tariffs, including sector-specific levies in Section 232 of the Trade Expansion Act of 1962.