Is the market too leveraged to AI and the Fed?

ANTHONY SAGLIMBENE – CHIEF MARKET STRATEGIST, AMERIPRISE FINANCIAL

WEEKLY MARKET PERSPECTIVES — NOVEMBER 17, 2025

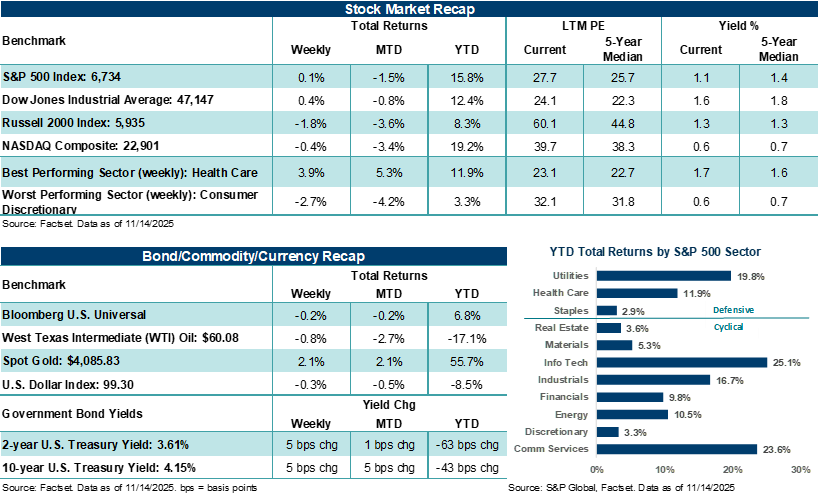

Major averages saw mixed performance during a volatile week of trading, as the odds of a December Federal Reserve rate cut fell, AI momentum was again called into question, and the longest U.S. government shutdown in history finally came to an end.

This week, NVIDIA’s highly anticipated earnings report is expected to shape investor perceptions on AI capital expenditure trends, demand dynamics, and equity leadership as the year comes to a close. FOMC October minutes, retail earnings reports, and the resumption of U.S. government economic data should keep market activity very fluid.

Last week in review:

-

The S&P 500 Index gained +0.1%, while the NASDAQ Composite fell 0.5%. AI scrutiny intensified after investors learned that Softbank sold its entire stake in NVIDIA (even though it is investing the proceeds in other AI companies), and credit spreads widened around AI capital expenditure projects.

-

The Dow Jones Industrial Average (+0.3%) and Russell 2000 Index (-1.8%) saw mixed performance across the week.

- The 43-day-long government shutdown ended midweek via a stopgap funding bill that will last until January 30. However, government data may trickle in slowly, and investors may have to deal with incomplete or missing data on employment and inflation through year-end. A December Fed rate cut is essentially a coin flip at the moment, given the limited economic data and more hawkish tones from Fed speeches last week.

- U.S. Treasury yields drifted higher. The U.S. Dollar Index was essentially flat, and Gold ended higher for the 11th week out of the past 13 weeks. West Texas Intermediate (WTI) crude posted a small gain after two consecutive weeks of decline, following OPEC projections that shifted from a supply deficit to a balanced market in 2026.

- Weekly ADP private payroll data showed a loss of roughly 11,000 jobs per week into late October, while the latest NFIB Small Business Index showed a step down in sentiment tied to hiring quality.

- American Express noted that Q4 billings trends are similar to those in Q3, and Bank of America reported that U.S. card spending increased by +2.4% year-over-year in October, the largest rise since early 2024. Bottom line: The debate between a bifurcated consumer, where high-income earners continue to spend, and low-to middle-income earners feel pinched, remains a prominent macroeconomic theme. The holiday shopping season, now underway unofficially, and retail earnings this week will likely be a good test of how durable this theme remains in 2026.

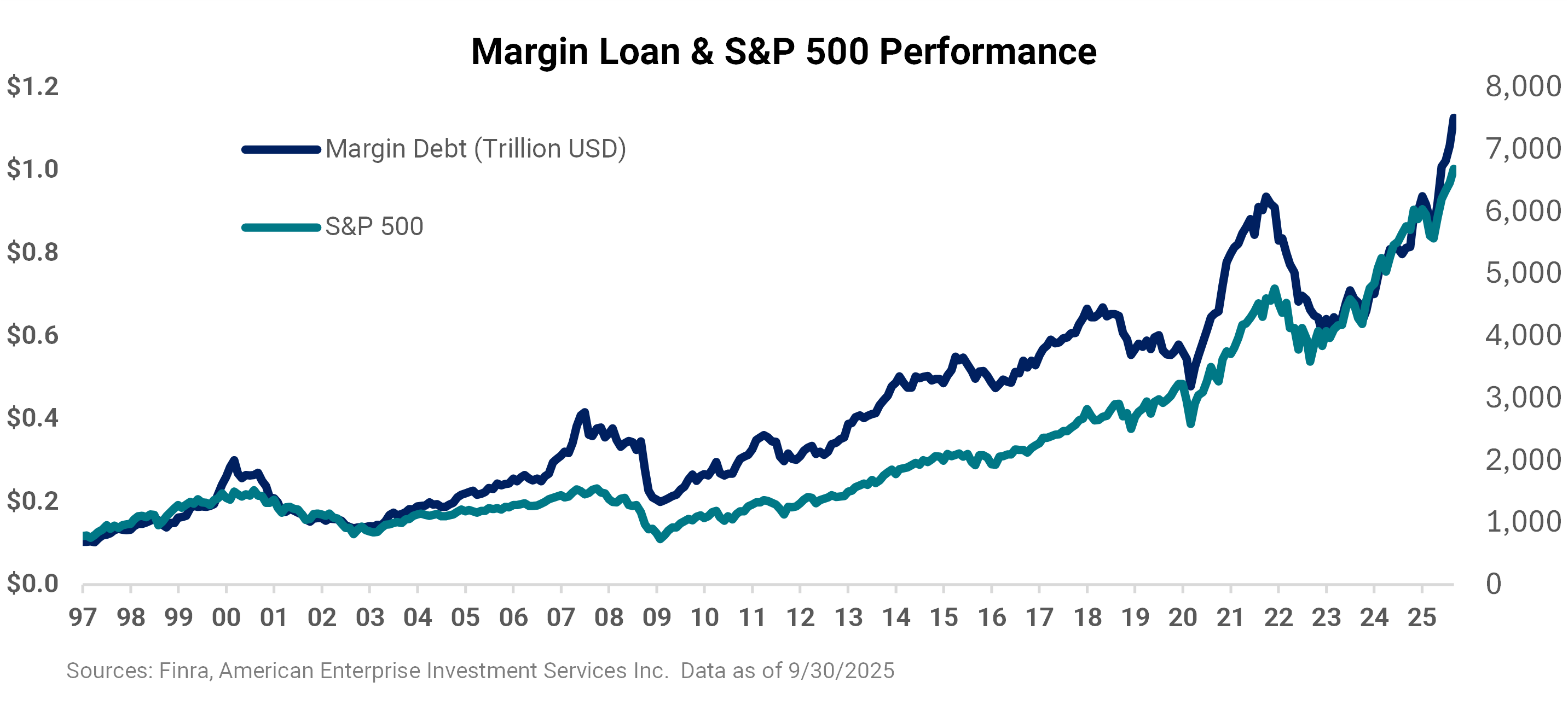

“Record margin debt is certainly a dynamic we are watching carefully, and it suggests that broader index moves could become sharper over time due to the increased use of leverage across the market. However, high margin debt alone is not a reason to deviate from a sound, well-thought-out and diversified investment strategy."

Anthony Saglimbene - Chief Market Strategist, Ameriprise Financial

Is the market too leveraged to AI and the Fed?

Investors spent last week repricing two key dynamics that could influence stock prices for the remainder of the year. The first is whether the Federal Reserve will cut rates next month. The second dynamic that prompted investors to reevaluate their thinking was the emergence of additional questions about the durability of AI-led leadership. Notably, enthusiasm around artificial intelligence faced added headwinds last week as investors questioned how quickly massive data center spending can translate into revenue (an ongoing concern as of late), while new concerns about the strength of company balance sheets tied to concentrated AI customers came under new light.

BCA Research noted that past capital expenditure waves can stumble (even if it’s for a short period within a longer-term arch of growth) when the adoption of a new technology follows ups and downs rather than a straight line. In addition, when pricing pressure compresses revenues more than expected (e.g., determining the useful life and replacement cycle of AI-related hardware), or when debt financing increases (as recent headlines suggest is happening within certain corners of AI), stocks have historically seen increased volatility. That is, asset prices tend to peak “before” investment cools, which can help explain why richly valued tech stocks have seen more volatility lately, as investors are beginning to draw sharper lines between announced capital expenditures, debt financing, and growing capacity versus monetizable demand.

On the Fed side, officials are now signaling a high bar for a December rate cut, which keeps the rate path uncertain heading into the last meeting of the year and has amplified stock sensitivity to the outlook for short-term rates. Notably, capex booms are most vulnerable when the cost of capital stops falling and adoption lags headlines. Something that’s not a problem today, but one that investors were thinking about last week, even if only briefly, and before stocks turned higher on Friday. Ultimately, earnings will need to do more of the heavy lifting to support elevated valuations across AI stocks. And the path forward for rate policy is likely to be lower, but perhaps not exactly on the timeframe most investors were hoping for. Given that government economic data is expected to start flowing again soon (e.g., the delayed September nonfarm payrolls report is anticipated to be released on Thursday), the odds for a December rate cut could change significantly between now and the December 10 decision.

Interestingly, with stocks still near all-time highs and some recent volatility casting a little doubt among investors, the question has shifted from whether the bull market can continue to what might challenge it. Notably, investor leverage is running hot, in our view. According to FINRA, margin balances hit $1.13 trillion in September, up +6.3% from August levels and nearly +39.0% higher from a year ago. September’s figure marked five straight monthly increases in margin debt, a sharp climb from May’s $921 billion. Nevertheless, we believe it’s the “pace” and “persistence” of this rise that matters most, as multi-month accelerations in the use of leverage often signal optimism that can make indexes more sensitive to surprises, both up and down.

For illustrative purposes only and is not guaranteed. An index is a statistical composite that is not managed. It is not possible to invest directly in an index. Past performance is not a guarantee of future results.

In our view, record margin balances alongside elevated valuations suggest a positive but cautious outlook, with a focus on position sizing and liquidity as key factors that could influence stock movements from here. History shows margin peaks can last while profits and liquidity remain supportive – an environment that is likely to persist heading into 2026. But the odds of sharper pullbacks rise when leverage is high and leadership is narrow. Breadth, or the number of stocks participating in gains, remains mostly concentrated in Big Tech stocks tied to AI. Breadth is a dynamic to watch if leadership remains narrow and leverage stays high. In this case, broad indexes could be more vulnerable to sharper pullbacks if AI-related stocks fail to meet expectations for an extended period. That said, if stock gains broaden into quality cyclicals, leverage may become less fragile to near-term disruptions.

Bottom line: Record margin debt is certainly a dynamic we are watching carefully, and it suggests that broader index moves could become sharper over time due to the increased use of leverage across the market. However, high margin debt alone is not a reason to deviate from a sound, well-thought-out and diversified investment strategy. In our view, the right response to added volatility is to stay invested through diversified ETFs, mutual funds and investment strategies, tilt toward quality companies that generate free cash flow (including in Technology), keep a modest cash cushion for opportunistic buying should weakness develop, and let fundamentals, particularly earnings strength, determine how much offense one plays in a market already at all-time highs. That approach can help keep one focused on the long game of owning secular leaders across areas like Technology, while providing one with practical tools to navigate a period where leverage, leadership, and valuation are all coming under added scrutiny.

The week ahead:

-

NVIDIA’s earnings report and outlook on Wednesday will likely be the event of the week, as it pertains to stock action. Investors will focus on the degree of demand for AI-related semiconductors (essentially a question of how much stronger or weaker that demand is compared to expectations), how management frames supply constraints, and trends in data center growth. Guidance on margins and capital spending could shape sentiment for the broader semiconductor space and stock market heading into year-end.

-

Reports from major retailers, including Home Depot, Lowe's, Target, and Walmart, will offer a read on consumer health, particularly discretionary spending versus essentials. Commentary on inventory levels and holiday outlooks will likely influence expectations for broader consumer health in the fourth quarter.

- The delayed September employment report will be released on Thursday, providing a much-needed update on job creation and wage trends. Labor market strength or weakness could recalibrate expectations for the Fed’s policy path heading into the December meeting.