A return to Fed rate cuts: What it means for your money

Brian Erickson, Fixed Income Strategist – Ameriprise Financial

November 12, 2025

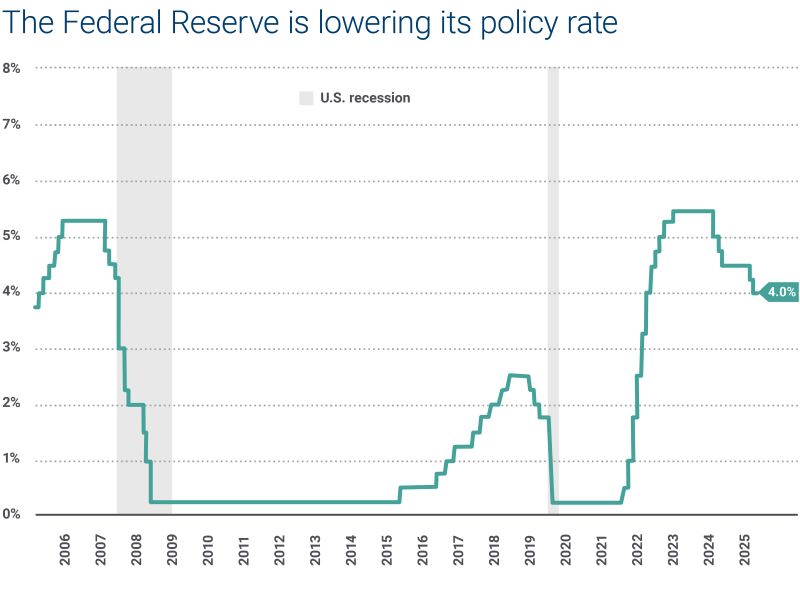

The U.S. Federal Reserve has begun to lower interest rates, signaling a shift toward easing monetary conditions.

How might this move impact your investments and financial position? Here’s our interest rate outlook.

What rate cuts could mean for the markets, economy and your money

The Fed uses interest rates to help guide the economy, raising them to cool economic activity or cutting them to encourage growth. Specifically, interest rate cuts aim to encourage spending and investment, which can have a ripple effect across the financial system. Here’s what this means for you:

-

Lower returns on cash: When the Fed cuts rates, returns on cash investments typically fall too. If you’re holding money in savings accounts or money market funds, you may start seeing lower yields.

-

Reconsider where you invest: As cash yields drop, it may be beneficial to start looking for better opportunities, like bonds, stocks or other income-generating assets. This shift can boost prices in many markets.

-

Floating-rate investments may pay less: If you own floating-rate bonds or loans, the income produced could decline as rates fall.

-

Cheaper borrowing for consumers and businesses: Lower rates mean it’s cheaper to borrow. Whether it’s a car loan, personal loan or business financing tied to the Secured Overnight Financing Rate (SOFR) or Prime Rate, borrowing costs generally decrease as rates decline.

-

Equity markets may react positively: Historically, lower rates have helped boost stock prices and narrow credit spreads.

-

Banks may benefit too: Banks that borrow at short-term rates and lend at longer-term ones could see improved profits as their interest margins widen.

Source: The Federal Reserve

What rate cuts don’t mean for the markets, economy and your money

While rate cuts can help jumpstart parts of the economy, they don’t fix everything. Macro concerns continue to influence how confident people feel about making long-term financial decisions:

-

Rate cuts do not necessarily translate to an immediate economic boost: It often takes some time for the broader economy to feel the effects of lower interest rates.

-

Macroeconomic dynamics may inhibit spending: Uncertainty around trade policy, inflation, and the job market can make businesses and consumers hesitant to invest or spend.

-

The labor market may remain challenging: AI’s impact on jobs and productivity is still unfolding, adding to the uncertainty. Thus, the impact of rate cuts on employment numbers may be somewhat muted.

-

If you are waiting for mortgage rates to fall, more patience may be required: Long-term borrowing costs, like 30-year mortgages or corporate bonds, are more influenced by inflation expectations than by short-term Fed moves.

As we enter the final quarter of 2025, Ameriprise Financial experts break down recent market and economic developments, including recent interest rate cuts. Get their projections on where the market may be headed in this episode of Ameriprise Talks. (9:20)

How might a new Fed chairman impact policy rates?

Jerome Powell’s term as chair of the Fed ends in May 2026, and that could mean a leadership change at the central bank.

The U.S. president chooses the next Fed chair, often someone already working in the Federal Reserve System or on its Board of Governors. The Senate must approve the president’s pick before they can assume the role.

The internal policies and procedures of the Fed place the chairman at the forefront but require a vote from a predetermined slate of voters at each Fed policy meeting. The current voting process has been in place since 1943 and was initially defined by the Federal Reserve Act of 1913. Any changes to the voting process (which is steeped in economic and historical tradition) require an act of Congress. As such, while there may be procedural nuances during the upcoming leadership transition, we expect to see continuity and stability in Fed policy execution.

How low could rates go?

The Fed has hinted that this round of rate cuts could mirror its last round of rate cuts in 2024. If that’s the case, we could see the Fed transition policy rates to a more neutral stance, closer to 3%. A 3% policy rate would position the Fed with greater flexibility to either tighten or ease policy as economic conditions evolve. However, for that scenario to transpire, inflation risks would need to be anchored to the Fed’s 2% long-term target.

Take advantage of the new interest rate environment

As interest rates ease, it’s a smart time to review your investment portfolio with your Ameriprise financial advisor. For example, you may consider exiting floating-rate and cash investments in favor of intermediate-term bonds or core bond funds, which may perform better in a falling rate environment.

Or, request an appointment online to speak with an advisor.

At Ameriprise, the financial advice we give each of our clients is personalized, based on your goals and no one else's.

If you know someone who could benefit from a conversation, please refer me.

Background and qualification information is available at FINRA's BrokerCheck website.