Bulls versus bears. Who will control the finish into year-end?

ANTHONY SAGLIMBENE – CHIEF MARKET STRATEGIST, AMERIPRISE FINANCIAL

WEEKLY MARKET PERSPECTIVES — NOVEMBER 24, 2025

Major U.S. stock averages experienced a rollercoaster ride amid key earnings reports and shifting expectations for Fed rate cuts last week. This week, a shortened holiday trading week, holiday shopping, and ongoing market gyrations will capture investors’ attention amid helpings of turkey and stuffing.

Last week in review:

-

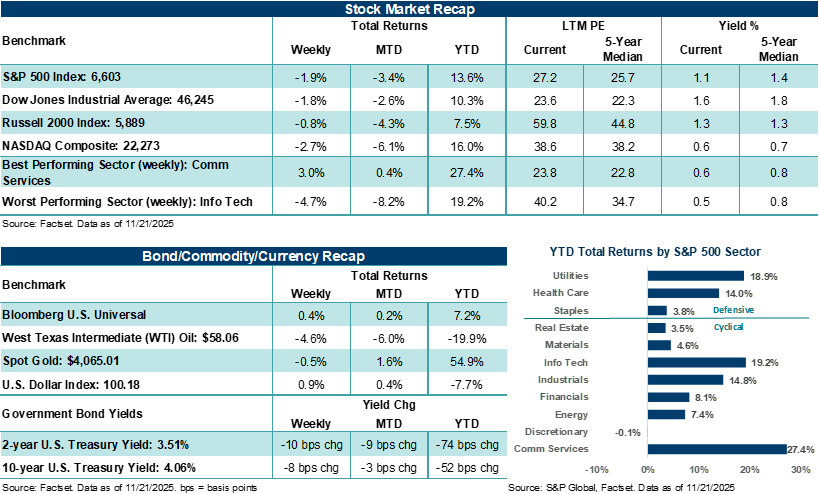

The S&P 500 Index (-2.0%) finished lower for a second week in the last three, while the NASDAQ Composite (-2.7%) ended lower for the third consecutive week. Alphabet ended up +8.0% on Gemini 3 enthusiasm, while Microsoft and Amazon fell sharply. The Dow Jones Industrial Average and Russell 2000 Index fell 1.9% and 0.8%, respectively.

-

U.S. Treasury prices were firmer across the curve, the U.S. Dollar Index rose, Gold ended lower, and West Texas Intermediate (WTI) crude finished down on the week.

- The delayed September nonfarm payrolls report surprised to the upside, but downward revisions erased August job gains. Continuing unemployment claims hit a two-year high.

- November preliminary manufacturing activity fell to a four-month low, while services activity rose to a four-month high. Input cost inflation accelerated to its fastest pace in three years, excluding May.

- Existing home sales posted their fastest pace of growth since February, while the final look at November University of Michigan sentiment was confirmed at the lowest level since mid-2022. That said, inflation expectations within the report eased at both 1-year and 5-year horizons, offering some relief on the inflation narrative.

- Although the October FOMC minutes leaned hawkish, New York Fed President John Williams later in the week signaled room for near-term rate cuts, which pushed December cut odds above 70% by Friday after odds for a December cut had fallen to 30% earlier in the week.

“While stock volatility may remain elevated in the near term, possibly due to some of the less-than-ideal conditions outlined in the bear case, the combination of strong earnings growth, ongoing innovation in AI, and a consumer still spending into the holiday season sets the stage for solid fundamental conditions heading into year-end.”

Anthony Saglimbene - Chief Market Strategist, Ameriprise Financial

Bulls versus bears. Who will control the finish into year-end?

Stocks continue to struggle in finding their footing, despite signs of clarity forming on some fronts. Investors digested a wave of high-profile reports last week, including NVIDIA’s standout results, a mixed bag from major retailers, and the long-awaited September nonfarm payrolls report. These updates arrived against a backdrop of heightened stock volatility in November, with Big Tech stocks continuing to come under pressure.

Notably, NVIDIA’s quarterly update was the clear highlight. The company beat revenue estimates by roughly $2 billion and guided next quarter’s sales nearly $3 billion above consensus. NVIDIA’s profit results and outlook last week pushed back on the idea of an AI bubble, underscoring that AI demand remains strong and is translating into tangible earnings. Yet, retail earnings painted a more mixed picture across consumers. Walmart posted strong results, beating expectations and raising its full-year sales growth forecast. However, there are growing signs of selective spending, with retailers such as Lowe’s and TJX delivering mixed but generally better-than-expected results and Target underscoring the unevenness in discretionary spending.

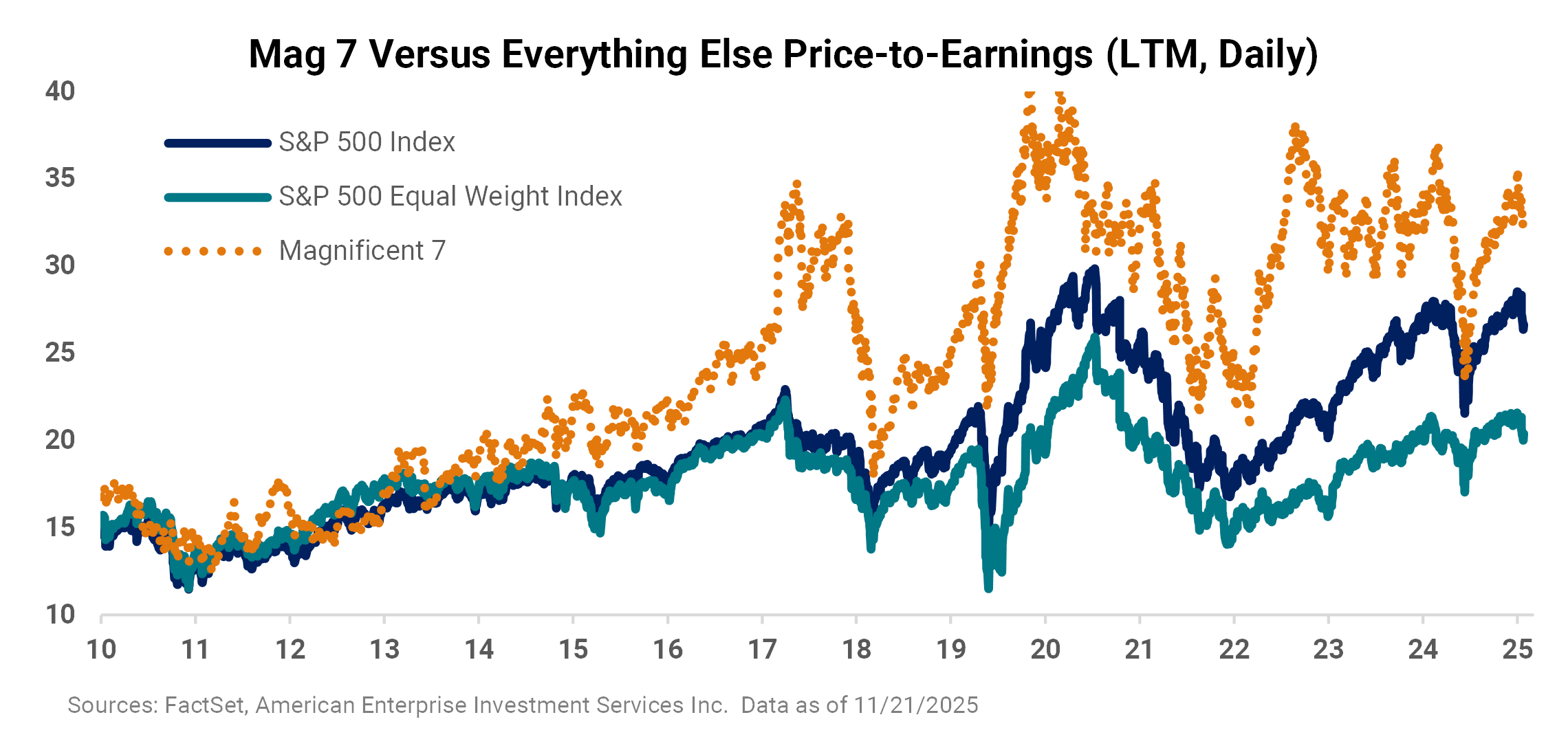

These figures are shown for illustrative purposes.

On the economic front, the September nonfarm payrolls report, delayed by the government shutdown, showed job gains of +119,000, well ahead of expectations, although prior months were revised lower. The unemployment rate ticked up to 4.4%, the highest in four years, and wage growth cooled. In our view, the report increases the likelihood that the Federal Reserve could hold its fed funds rate steady next month. However, as last week's developments indicate, the odds of a December cut can change quickly. With all that backdrop out of the way and stock volatility running higher, we thought it would be helpful to provide a look at the bullish and bearish items we are currently keeping our eye on to frame current conditions.

Bull case for stocks heading into year-end:

- We believe strong demand for AI infrastructure is driving tangible earnings growth now and into the future. For example, NVIDIA’s Q3 results and forward guidance exceeded consensus by meaningful amounts, with management highlighting robust demand from both sovereign and hyperscale customers. Despite concerns about valuations and capex spending, the fundamental picture for Big Tech looks strong heading into 2026.

- Speaking of Big Tech, Google’s recent Gemini 3 launch reflects only the most recent example of AI innovation and positive application development, countering the skepticism narrative. The model’s top scores on industry benchmarks and favorable analyst commentary suggest that the AI theme should remain a central driver for technology stocks well into next year.

- Retail sector leaders like Walmart are delivering solid results amid a more complex economic backdrop, with U.S. comps up +4.5% in Q3 and eCommerce momentum accelerating. Although consumer spending remains bifurcated and shows signs of strain among lower-income households, the overall consumer backdrop heading into the holiday shopping season appears positive and points to spending growth through year-end.

- In our view, Federal Reserve easing remains a key piece of the macroeconomic narrative. Despite more volatile pricing for a December rate cut, the market is still pricing in around 90 basis points of rate cuts through year-end 2026. The latest FOMC minutes and recent Fed commentary suggest that most officials anticipate further rate cuts over time, providing a supportive backdrop for equities.

- Recent stock weakness has somewhat helped ease stretched stock valuations. In addition, hedge fund net leverage has decreased to levels that have historically served as a “floor,” and retail investors remain active. Stock trading on Thursday and Friday may be a positive signal for market resilience.

- Finally, seasonality could provide a tailwind. Historical data shows that when the S&P 500 is negative month-to-date into Thanksgiving, the final weeks of the year often see a rebound, with average gains of nearly +3.0% through Christmas and +4.0% through New Year’s Eve, according to Jefferies.

Bear case for stocks heading into year-end:

- AI scrutiny and skepticism continue to hold firm, with investor concerns regarding capital constraints, capex sustainability, and widening credit spreads. Questions around the circularity of financing among AI leaders and lingering uncertainty about return on investment are prompting investors to reassess the durability of the AI trade.

- Short-term technical pressure has mounted this month, with the S&P 500 and NASDAQ Composite temporarily breaking below key moving averages, like the 100-day. Stocks could remain more volatile in the near term, as traders and short-term investors test and confirm technical support levels.

- FOMC minutes reveal a divided Fed, and the lack of clear direction on monetary policy, combined with messy economic data, could keep stock volatility elevated and limit the upside for equities through year-end.

- Private credit concerns are simmering in the background, with high-profile fund mergers (Blue Owl) scrapped and portfolio declines (BlackRock) triggering over-collateralization breaches.

- Global liquidity is under pressure, with rising long-term yields in Japan and deficit concerns in the UK and elsewhere acting as a drag on popular trading strategies, including AI and technology stocks.

- Retail earnings outside of Walmart have been mixed to negative. Home Depot and Target both reported disappointing results, with weaker comparable sales, margin compression, and cautious guidance, pointing to ongoing consumer uncertainty and margin headwinds.

Bottom line: While stock volatility may remain elevated in the near term, possibly due to some of the less-than-ideal conditions outlined in the bear case, the combination of strong earnings growth, ongoing innovation in AI, and a consumer still spending into the holiday season sets the stage for solid fundamental conditions heading into year-end, in our view. Importantly, considering that major averages like the S&P 500 and the NASDAQ Composite remain on pace to post their third consecutive year of annual double-digit returns, it’s reasonable to expect that stocks will experience periods of pressure from time to time, which, historically, is quite healthy for longer-term strength.

The week ahead:

-

Due to the U.S. government shutdown, there will not be an October CPI release, and it is unknown when/how the Fed’s preferred measure of inflation, core PCE, will be released by the Bureau of Economic Analysis. However, investors will receive a delayed look at September producer inflation on Tuesday. In addition, a second look at Q3 GDP on Wednesday and housing data throughout the week line the economic calendar.

-

U.S. markets are closed for the Thanksgiving holiday on Thursday and will close early at 1 pm EST on Friday. Adobe Analytics projects that Americans will spend $43.7 billion online from Thanksgiving Day through Cyber Monday, up +6.3% annually and representing roughly +17.0% of all online holiday spending. Adobe also projects that total 2025 online holiday spending (from November 1st through December 31st) will reach $253.4 billion, up +5.3% year-over-year.