How far can one engine take the market?

ANTHONY SAGLIMBENE – CHIEF MARKET STRATEGIST, AMERIPRISE FINANCIAL

WEEKLY MARKET PERSPECTIVES — MAY 4, 2026

U.S. equities extended their advance for a fifth consecutive week, with the S&P 500 Index and NASDAQ Composite closing at fresh all-time highs, as Q1 earnings growth accelerated sharply and Big Tech results broadly reinforced a positive AI investment narrative. However, a divided Federal Reserve and an unresolved Middle East stalemate played in the background. This week, jobs data and a busy slate of Q1 earnings reports will be in focus.

Last week in review:

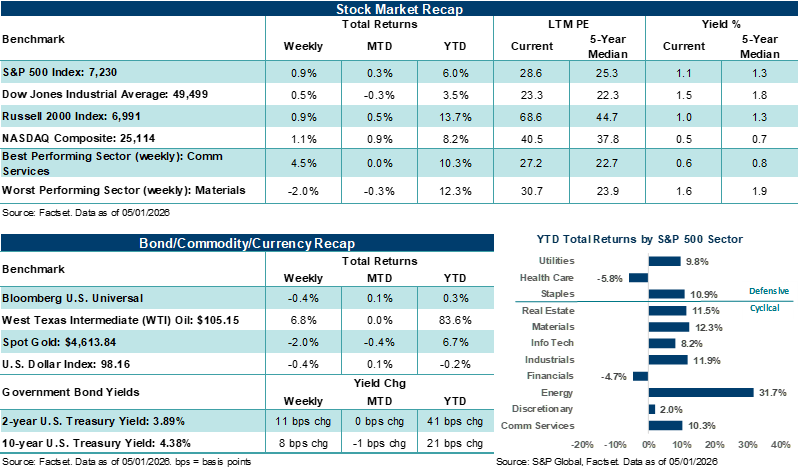

- The S&P 500 gained +0.9%, while the NASDAQ rose +1.1%. The Russell 2000 advanced +0.9%, its sixth consecutive weekly gain, and the Dow Jones Industrial Average gained +0.5%.

- Communication Services and Energy led all S&P 500 sectors, gaining +4.5% and +3.2%, respectively. Materials were the notable laggard, falling nearly 2.0%.

- Treasury prices weakened, and the U.S. Dollar Index declined, with yen strength the big FX story on intervention headlines. Gold finished lower, and West Texas Intermediate (WTI) crude rose +6.8%, adding to the prior week's +14% gain as physical supply conditions continued to tighten.

- U.S./Iran headlines remained noisy, the Strait of Hormuz remains closed, but the ceasefire continues to hold.

- Q1 earnings were the dominant focus outside the Federal Reserve meeting, with more than 60% of S&P 500 constituents having now reported. Big Tech results were broadly supportive of the AI theme, though elevated capital spending plans continued to draw scrutiny across the group. Outside of mega-cap tech, software earnings helped ease AI disruption fears, memory delivered strong results and select industrials beat on backlog and bookings strength. Payment processors reinforced the consumer resilience narrative, though pockets of consumer-facing weakness surfaced in digital entertainment and select restaurants.

- As expected, the Federal Reserve held its rate policy unchanged, but the meeting was marked by rare internal division, with four dissents.

- Economic data was broadly supportive last week, with GDP rebounding from Q4's sluggish pace, cooling inflation, and the labor market showing continued resilience.

“We believe the AI engine is powering corporate earnings, business spending and equity returns. Clear reasons why stocks are sitting at fresh new highs to start the week. And while the consumer engine is still running, supported by low layoffs and a stable unemployment rate, we hear some engine knocks forming. If this week's employment data shows the labor market is holding firm, the rally may have more room to extend into the summer. If it doesn't, investors may have to confront the risks of an investment environment that doesn't run as efficiently as the stock market might imply.”

Anthony Saglimbene - Chief Market Strategist, Ameriprise Financial

How far can one engine take the market?

In April, we believe one of two engines principally carried the equity market to its best month since November 2020, powered Q1 GDP growth, and drove earnings beats across every major hyperscaler. Unsurprisingly, that engine is artificial intelligence. Conversely, the other engine, the American consumer, is still firing but might be starting to run low on fuel. This week's employment data should help determine how far the first engine can take markets without the second running at full strength.

Notably, the S&P 500 Index gained +10.4% in April, its best month since the COVID-19 vaccine breakthrough in November 2020. The NASDAQ Composite rose +15.3% last month, its best month in six years. Semiconductors led the way, with the Philadelphia Semiconductor Index gaining over +38%, its strongest month since February 2000. Inside Big Tech, Alphabet led the Magnificent Seven at nearly +34%, with Amazon up over +27%. The same AI engine was hard at work across the Pacific as well. South Korea's Kospi closed at a record, with chip manufacturing accounting for more than half of the country's Q1 GDP growth, per the Korea International Trade Association. Taiwan's TAIEX topped 40,000 for the first time last month. Japan's Nikkei breached 60,000 for the first time in its history. And on the flow front, Goldman Sachs estimated that certain trading strategies purchased $80 billion in U.S. equities over the past month, the second-highest on record. However, we believe that mechanical bid to buy stocks might have run its course, with Goldman also noting that May has historically been the largest outflow month of the year for equity mutual funds and ETFs. That said, the reopening of the buyback window following the reporting season could provide an offset.

The AI engine, back to running on all cylinders, was also visible in the economic data last week. Q1 GDP grew at a +2.0% annualized rate, and AI-linked business investment did most of the work. Equipment and intellectual property spending rose at a +10.4% pace, the fastest in nearly three years. Pantheon Macroeconomics estimated AI investment accounted for roughly half of overall GDP growth. Federal government spending also contributed to growth in Q1, but that was a one-time snapback from Q4's government shutdown-driven contraction and is unlikely to repeat. Take AI out of the equation, and the economy barely grew.

On that point, the consumer side shows the engine might not be firing on all cylinders at the moment. Spending decelerated to a +1.6% annualized pace in Q1 from +1.9% in Q4 2025. The PCE Price Index jumped to +3.5%, up from +2.8%, reflecting the pass-through of higher energy costs. For example, gas prices hit $4.39 per gallon on Friday, per AAA, the highest since July 2022. And according to Bank of America, the gas price spike since the Iran conflict began has already cost consumers an estimated $19 billion, eroding nearly half of the $43 billion boost from higher tax refunds this filing season. In addition, the personal savings rate fell to 3.6% in March, according to the Bureau of Economic Analysis, the lowest level in over three years, while the University of Michigan's Consumer Sentiment Index dropped to a record low in April. That said, the picture is not uniformly negative. Visa noted growth across consumer spending bands saw incremental improvement in Q1, with no signs of weakening among lower-spend consumers. Mastercard echoed that view in its earnings report, citing healthy underlying spending despite elevated geopolitical risks.

In our view, the consumer engine is still running, but it's running without a full tank of gas. Importantly, this isn't just a domestic dynamic, in our view. Every major central bank that met last week held rates steady and leaned hawkish. The European Central Bank signaled a June rate hike is on the table, while the Bank of England held rates steady, with four members close to supporting a hike. For its part, the Bank of Japan saw three dissenters favor a rate hike and intervened in currency markets for the first time since 2024. Bottom line: Energy-driven inflation is straining the consumer engine globally.

Here at home, last week's Federal Reserve decision mapped directly into this theme. The FOMC held rates at 3.50% to 3.75%, as expected. But the 8-4 vote, the most divided since October 1992, revealed a split within the committee over which engine to protect. Governor Miran dissented in favor of a rate cut, prioritizing the labor market. Hammack, Kashkari, and Logan supported the hold but opposed the statement's easing bias, prioritizing the inflation engine. The majority of governors retained the easing bias, but Chair Powell acknowledged it was a "closer call" than in March. Notably, Powell also flagged that the Fed cannot simply look through the current energy shock the way it traditionally would, given inflation has been above target for several years, and the committee is already looking through the tariff shock. Markets are now pricing zero rate cuts through year-end. Powell confirmed he will remain on the Board of Governors after his term ends on May 15, adding a layer of institutional tension as Kevin Warsh prepares to take the helm as Chair. Bottom line: Warsh will soon inherit a committee where the debate has shifted from when to cut rates to whether the committee should be signaling cuts at all.

On the earnings front, Amazon, Alphabet, Meta Platforms, and Microsoft beat profit estimates last week, and cloud growth accelerated across every hyperscaler. The broader Q1 earnings season has been very strong from our vantage point. The S&P 500 blended earnings per share growth rate ended the week at roughly +27% year-over-year, up from +12.6% at the start of the reporting season, per FactSet. The market's response to Mag Seven reports was also instructive, in our view. Companies demonstrating clear returns on AI investment were rewarded. Those still asking investors to be patient with rising costs were not. Simply, the AI engine is running well, but the market demands fuel efficiency, not just horsepower. In our view, Apple's results may be the single best barometer of the divide between engines. Services revenue, the AI-adjacent business, topped estimates. iPhone sales, tied to consumer wallets, came in short of expectations.

Importantly, this week’s labor market update might be where the two engines converge. Tuesday's JOLTS report will show whether job openings continued to decline in March. Importantly, the ratio of openings to unemployed workers fell to 1.02 in February, barely above 1:1. A move below that level would mark the first time since the pandemic recovery that job seekers outnumber available positions. Wednesday brings ADP private payrolls for April, and Friday will be the main event with the April nonfarm payrolls report on tap. FactSet estimates point to just +50,000 jobs created in April, with the unemployment rate seen holding steady at 4.3%. Recall that March came in at +178,000, though that figure was inflated by roughly +35,000 Kaiser Permanente workers in California and Hawaii returning to payrolls after a four-week strike. In our view, an April reading below +50,000 could raise investor concerns quickly, but a print in the neighborhood around +100,000 could help demonstrate consumer resilience.

Bottom line: We believe the AI engine is powering corporate earnings, business spending, and equity returns. Clear reasons why stocks are sitting at fresh new highs to start the week. And while the consumer engine is still running, supported by low layoffs and a stable unemployment rate, we hear some engine knocks forming. If this week's employment data shows the labor market is holding firm, the rally may have more room to extend into the summer. If it doesn't, investors may have to confront the risks of an investment environment that doesn't run as efficiently as the stock market might imply. As we often note, maintaining a balanced approach and avoiding overly bullish or bearish views is prudent when navigating sometimes contradictory signals, or in this case, when the check engine light pops on.

The week ahead:

-

25% of the S&P 500 will report Q1 results this week, including reports from Palantir, Pfizer, Walt Disney, and McDonald’s.

-

April ISM Services hits on Tuesday, with activity expected to expand for the 22nd month in a row.

- A preliminary look at May University of Michigan consumer sentiment on Friday is expected to remain at record-low levels.