Is recent AI pressure and Fed uncertainty setting the stage for 2026?

ANTHONY SAGLIMBENE – CHIEF MARKET STRATEGIST, AMERIPRISE FINANCIAL

WEEKLY MARKET PERSPECTIVES — NOVEMBER 10, 2025

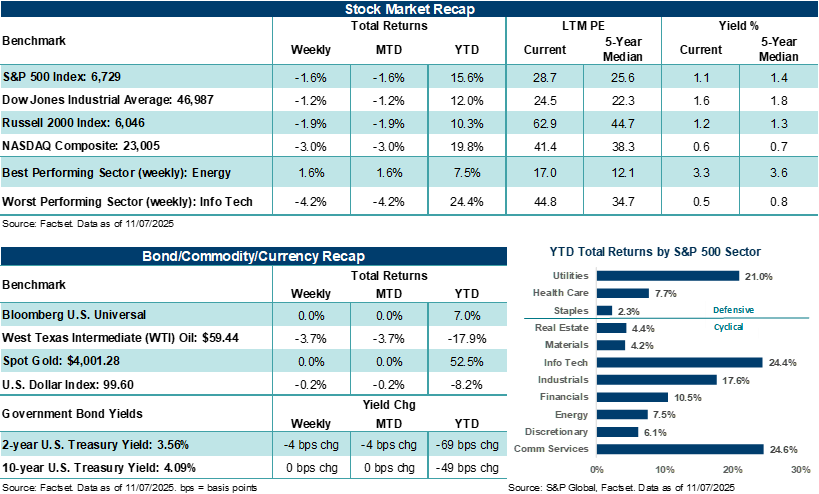

Major U.S. stock averages declined last week as scrutiny on AI intensified and policy uncertainty in Washington and around the Federal Reserve weighed on investor sentiment. However, last week’s decline in the S&P 500 Index and NASDAQ Composite follows three straight weeks of gains. This week, investors will continue to monitor Big Tech trends, Fed speeches, and the timing of economic releases as the U.S. government prepares to reopen.

Last week in review:

-

The S&P 500 Index and NASDAQ Composite dropped 1.6%, and 3.0%, respectively. Big Tech was under pressure last week, with NVIDIA falling 7.0%, Tesla dropping 5.9%, and Meta Platforms falling 4.1%. AI scrutiny was the major theme weighing on the broad indexes last week, as investor concerns regarding cash burn, leverage, circularity of deals and agreements, and return on investment pushed back against elevated valuations. Bottom line: Big Tech stocks have been running higher for months, and it's quite healthy and normal in our view to have some rationalization around forward expectations. We expect the major averages to face some near-term headwinds if investors continue to exert pressure on Big Tech stocks heading into NVIDIA’s closely anticipated earnings report on November 19. That said, we don’t see recent pressure in the AI arena changing the overall longer-term positive narrative encompassing the advanced technology and/or the stocks that are building out the infrastructure.

-

The Dow Jones Industrial Average and Russell 2000 Index lost 1.2% and 1.9%, respectively.

- U.S. Treasury prices were mostly firmer across the curve, the U.S. Dollar Index declined, and Gold stabilized around $4,000 per ounce. However, the precious metal finished the week about 8.0% below its all-time high set on October 20. West Texas Intermediate (WTI) crude dropped 2.0% on the week.

- On the economic front, given that U.S. government releases are delayed due to the ongoing shutdown, private data is carrying increased weight with investors at the moment. Challenger job cuts hit more than 150,000 in October, the most in two decades, while University of Michigan consumer sentiment unexpectedly declined this month to its worst level since June 2022. ISM manufacturing and services activity showed mixed results on the U.S. economy last month, while October ADP private payrolls data beat forecasts and turned positive for the first time in two months.

- Effects from the longest U.S. government shutdown in history intensified, with the Federal Aviation Administration (FAA) canceling flights on Friday to ease pressure on air traffic controllers, and delayed SNAP benefits began to take their toll on lower-income households that rely on such benefits to feed their families. Headlines going into the weekend suggested that Democrats and Republicans were starting to engage in talks in an effort to find a resolution to their impasse, which they did find on Sunday. The Senate passed legislation to reopen the government and fund federal agencies through January.

- Odds for a 25-basis point Fed rate cut next month remain skewed toward the Fed cutting. Still, the cut may remain a game-time decision for policymakers, given the current lack of available government data.

“So, why does the last Fed meeting of the year matter so much? Because the Fed’s updated projections will frame the policy path for 2026. In our view, markets are less concerned with whether the Fed cuts in December than with whether policymakers confirm a glide path toward lower rates next year.”

Anthony Saglimbene - Chief Market Strategist, Ameriprise Financial

Is recent AI pressure and Fed uncertainty setting the stage for 2026?

As noted above, major U.S. stock averages ended last week lower, with the S&P 500 and NASDAQ Composite retreating after labor data signaled further cooling, and scrutiny on AI valuations intensified. The Challenger jobs report showed that October layoffs were roughly three times the year-ago level, with cumulative cuts this year reaching one million. In addition, ADP private payrolls posted only modest gains last month, concentrated in large firms, while smaller companies slowed hiring. Notably, services activity in October expanded with the strongest new orders in a year, but employment contracted, and input prices stayed elevated. On the manufacturing side, activity remained in contraction, though orders and hiring improved slightly. In the absence of government data, due to the shutdown, investors were reminded that the U.S. economy remains on a two-track tier and labor conditions are softening.

On the market side of the equation, Technology stocks faced renewed valuation pressure last week as investors reassessed AI spending timelines, with semiconductors under added scrutiny for margin durability and 2026 supply ramps. For example, Qualcomm and AMD faced pressure following solid earnings reports, as some investor fatigue may be setting in after months of strong gains across semiconductor stocks. That said, even in a down market, broader market trends improved beneath the surface, with Energy, Healthcare, and Financials outperforming Technology and Communication Services. Despite the added volatility, we remain constructive on year-end performance for the major averages and view the recent downdraft as healthy and warranted, assuming expectations for earnings growth in Q4 and early next year don’t dip below the usual current quarter adjustments.

Notably, the December Federal Reserve meeting could be one of the last major focal points of the year for investors. Policymakers have cut rates twice this year by 25 basis points each, and another 25-basis-point cut next month is likely to be a close call. A rate cut could reinforce a gradual shift toward easier conditions heading into next year, favoring rate-sensitive sectors and long-duration growth areas, such as Technology. A pause in rate cuts next month, with language keeping future cuts on the table, could still support markets, though we expect markets to become choppier heading into year-end. Regardless, Fed Chair Powell’s messages and tone after the meeting, as well as the updated Summary of Economic Projections, will matter as much as the decision itself.

So, why does the last Fed meeting of the year matter so much? Because the Fed’s updated projections will frame the policy path for 2026. In our view, markets are less concerned with whether the Fed cuts in December than with whether policymakers confirm a glide path toward lower rates next year. If inflation continues to cool and labor market conditions avoid sharp deterioration, the Fed’s own forecasts indicate a gradual shift toward neutral rates. Historically, stocks have performed well when interest rates decline gradually during an economic expansion, as lower borrowing costs support investment and valuations without undermining confidence in economic growth. We believe that’s the scenario investors want to see reinforced next month.

A December rate cut paired with guidance for further easing would likely extend the rally into year-end and broaden participation beyond Big Tech. Even a pause, if paired with language that keeps the door open for cuts, can support sentiment, in our view. The nuance is that markets look six to nine months ahead. By the time a cut is made, much of the benefit is already reflected in stock prices. That’s why the Fed’s “signal” for 2026 matters as much as the December rate decision.

A clear path toward lower rates next year, coupled with steady inflation progress, is historically a recipe for solid stock conditions. However, two factors, beyond the Fed, will likely determine whether that backdrop translates into higher stock prices: Earnings and breadth. The advance higher in stocks and major U.S. averages in recent years has leaned heavily on mega-cap Tech and early AI spending. For the next leg higher in the bull market, investors will likely want to see those investments convert into revenue and cash flow gains across cloud, software, semiconductors, and companies and industries that adopt or spend on AI. If that proof is established, reliance on multiple expansion could fade, and more sectors could join the rally as interest rates continue to decline and profit growth expands.

However, if inflation stalls above the Fed’s comfort zone, policymakers could slow the pace of cuts or pause longer next year, lifting yields and pressuring rate-sensitive areas. And if labor conditions further weaken, forcing aggressive rate cuts, investors may shift focus from rate support to the earnings hit that often accompanies slower demand environments. Of course, tariff and regulatory headlines could also inject volatility into the stock narrative next year, independent of Fed policy. Still, the overarching connection between monetary policy and equities is pretty straightforward: Steady easing paired with stable growth has historically allowed rallies to extend and broaden. As we head into year-end and begin thinking about the path forward for next year, that remains the lens through which we are starting to frame our outlook.

The week ahead:

-

Big Tech could face near-term challenges as investors look ahead to NVIDIA’s profit report next week (which should be solid in our view), and as AI spending, future profitability, and valuation concerns come under added scrutiny. Investors will likely also monitor this week how market breadth develops and whether stock volatility does creep higher. If so, can other areas of the market hold up?

-

Once the U.S. government is back open, investors will quickly turn their attention to how fast major economic data is released to assess current economic conditions and get a gauge on where key trends on labor and inflation are heading. Federal Reserve speeches and Treasury auctions this week will be in focus until government data starts rolling in.

- Notably, the Federal Reserve’s policy path (as discussed above) and tariff developments (i.e., the pending Supreme Court decision on President Trump’s emergency powers) will likely remain background items that investors will continue to consider in their U.S. growth, inflation, and equity valuation calculations. In our view, strong consumer and business balance sheets, along with AI-driven investment, continue to support earnings. However, elevated valuations and trade uncertainty warrant grounded expectations.